Where Does the Money Go in a Dual Income Family?

As I mentioned before, Harvard Magazine almost always has an unintentionally enlightening article, one that makes you say, "Well, yes, follow that thought through and you might get somewhere." Typically it concerns some issue where social science is demonstrating a deletrious effect of lifestyle changes which the magazine is compelled by its political stance to treat as beyond question.

So it is in this case.

In an article by Elizabeth Warren, the author talks of the "Middle Class on the Precipice," specifically referring to the dual-income family. Her argument is that the dual-income family model of economic life is far less secure than the former single-income family model that prevailed until 1970 or so.

Scholars, policymakers, and critics of all stripes have debated the social implications of these changes, but few have looked at their economic impact. Today the median income for a fully employed male is $41,670 per year (all numbers are inflation-adjusted to 2004 dollars)—nearly $800 less than his counterpart of a generation ago. The only real increase in wages for a family has come from the second paycheck earned by a working mother. With both adults in the workforce full-time, the family’s combined income is $73,770—a whopping 75 percent higher than the median household income in the early 1970s.

One good point the article makes is a single-income family can respond to a loss of the breadwinner's income (for whatever reason: death, injury, laid-off, fired, etc.) by sending the other parent into the paid labor force. Dual-income families don't have that option. In other word, single-income families work with a kind of discipline of deliberately keeping half of its potential labor force in reserve "for a rainy day," so to speak.

She also points out the tilting of the balance in the credit market from the debtors to the creditors, aided by Congress:

Since the early 1980s, the credit industry has rewritten the rules of lending to families. Congress has turned the industry loose to charge whatever it can get and to bury tricks and traps throughout credit agreements. Credit-card contracts that were less than a page long in the early 1980s now number 30 or more pages of small-print legalese. In the details, credit-card companies lend money at one rate, but retain the right to change the interest rate whenever it suits them. They can even raise the rate after the money has been borrowed—a practice once considered too shady even for a back-alley loan shark. When they think they have been cheated, customers can be forced into arbitration in locations thousands of miles from home. Some companies claim that they can repossess anything a customer buys with a credit card.

Smart people will avoid credit-card debt like dead birds in Turkey, but lots of people aren't smart, and the Bible tells us that God hates, yes HATES those who take advantage of their naivete. Even though they failed, we should be thankful for men like retired congressman Henry Hyde who tried to speak up for the debtors in the new bankruptcy law (and I know about the fraudulent use of bankruptcy; I know of a local millionaire of notoriously lax business ethics who regularly uses it to get out of inconvenient debts. Throw the book at him and people like him, but don't wink at the credit companies' loan sharking practices.)

Professor Warren also makes a good point about retirement risk being shifted on to the backs of families:

During the same period, families have been asked to absorb much more risk in their retirement income. In 1985, there were 112,200 defined-benefit pension plans with employers and employer groups around the country; today their number has shrunk to 29,700 such plans, and those are melting away fast. Steelworkers, airline employees, and now those in the auto industry are joining millions of families who must worry about interest rates, stock market volatility, and the harsh reality that they may outlive their retirement money. For much of the past year, President Bush campaigned to move Social Security to a savings-account model, with retirees trading much or all of their guaranteed payments for payments contingent on investment returns.

Now with these issues of retirement we have to remember that a defined benefit plan isn't a human right or a gift from heaven. Like many of the institutions that buttressed the security of the single-income families in the 1950s and 1960s they were created by unions, reformers (mostly women), and Democratic administrations who were animated by the ideal of the secure, home-centered, single-income family. (You can read more about this lost legacy of pro-family activism here.) Sadly their efforts were not accompanied by a similar focus on creating a pro-family culture, and so the result of the security and stability of the fifties was to create a generation that took it all for granted (Jeshurun grew fat and kicked . . .)

But unfortunately a good part of her article also aims to make the case that the dual-income model is irreversible (of course!), and driven by "rising prices for essentials as men’s wages remained flat." Actually though, the statistics she presents tell quite a different story. The only essential item that people are spending more on (and boy, are they spending more on it!) is housing. The only other major increases in the average budget are taxes, child care, and cars.

First she argues that families today are not living more luxuriously than in 1970; they are actually spending less on clothing, food, and household applicances:

. . . the average family of four today spends 33 percent less on clothing than a similar family did in the early 1970s. Overseas manufacturing and discount shopping mean that today’s family is spending almost $1,200 a year less than their parents spent to dress themselves. . . . Today’s family of four actually spends 23 percent less on food (at-home and restaurant eating combined) than its counterpart of a generation ago. The slimmed-down profit margins in discount supermarkets have combined with new efficiencies in farming to cut more costs for the American family. Appliances tell the same picture. . . . manufacturing costs are down, and durability is up. Today’s families are spending 51 percent less on major appliances than their predecessors a generation ago.

Even when we factor in the "23 percent more—a whopping extra $180 annually" spend on entertainment and the $300 more spent on computers, the total spent on all the above mentioned items combined is less for today's dual-income family that it is for 1970's single income family.

It's worth interjecting here that the savings in food and clothing are something which we can attribute to the Wal-Marts and Sam's Clubs of the world. Greater efficiency in the retail market has made a real difference to peoples' incomes.

So why are families today spending so much more? In a word, bigger houses and higher taxes, although the author struggles mightily to obscure the fact:

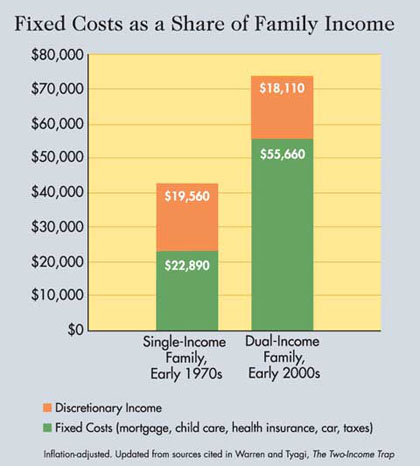

The data can be summarized in a financial snapshot of two families, a typical one-earner family from the early 1970s compared with a typical two-earner family from the early 2000s. With an income of $42,450, the average family from the early 1970s covered their basic mortgage expenses of $5,820, health-insurance costs of $1,130 and car payments, maintenance, gas, and repairs of $5,640. Taxes claimed about 24 percent of their income, leaving them with $19,560 in discretionary funds. That means they had about $1,500 a month to cover food, clothing, utilities, and anything else they might need—just about half of their income.

By 2004, the family budget looks very different. As noted earlier, although a man is making nearly $800 less than his counterpart a generation ago, his wife’s paycheck brings the family to a combined income that is $73,770—a 75 percent increase. But higher expenses have more than eroded that apparent financial advantage. Their annual mortgage payments are more than $10,500. If they have a child in elementary school who goes to daycare after school and in the summers, the family will spend $5,660. If their second child is a pre-schooler, the cost is even higher—$6,920 a year. With both people in the workforce, the family spends more than $8,000 a year on its two vehicles. Health insurance costs the family $1,970, and taxes now take 30 percent of its money. The bottom line: today’s median-earning, median-spending middle-class family sends two people into the workforce, but at the end of the day they have about $1,500 less for discretionary spending than their one-income counterparts of a generation ago.

Let's put this in tabular form in order of decreasing magnitude:

Mortgage then: $5,820; now: over $10,500 > + over $4,680

Taxes then: $10,188 (24% of income); now: $22,131 (30%) > +11,943 [since we generally agree taxes should be proportional to income this is misleading; had the tax rate stayed 24% per average family, today's tax bill would have been $4,426 lower].

Health insurance then: $1,130; now: $1,970 > +840

Even I was rather astounded by how really insignificant health insurances increases are compared to tax increases.

The other increasing expenditures -- for child care and for a second car -- are (at least in part) entailed by the decision to be a dual-income family:

Child care expenses then: $170*; child care expenses now: $5,660 (school age) -$6,920 (pre-school) > +$5,490 to $6,750

Car expenses then: $5,640 (for one car); now: over $8,000 (for two) > + over $2,360 [note the apparent implication that in real terms cars have gotten cheaper]

So while Professor Warren concludes that the dual-income family is a victim of forces beyond its control, and will eventually demand political action to reduce risk, what I conclude is that:

1) As long as you are willing to live in a small house and own one car, the single-income family makes as much sense as it ever did.

2) The desire for bigger houses is the main driving force behind the dual-income family.

And I can't avoid another query: is the flood of relatively unskilled female workers into the labor market keeping wages soft?

Tim Bayly has put up a very interesting post on big houses here. He questions why families with fewer children need more space. And if they don't need it, is it not squandering to buy it? What he doesn't mention is Isaiah 5:8-9:

Woe unto them that join house to house, that lay field to field, till there be no place, that they may be placed alone in the midst of the earth! In mine ears said the LORD of hosts, Of a truth many houses shall be desolate, even great and fair, without inhabitant.

Why woe to them? Because they have done injustice to seize other men's fields? Certainly. But is there not something antisocial in the very desire to "be placed alone in the midst of the earth"? And does not the desire for bigger houses drive the desire to move to the outskirts of town, which makes a second car necessary, thus creating the other big drain on the family income?

My conclusion is hopeful, though: economize on your house, and don't buy a second car, and a single-income family has a realistic chance of achieving the financial security and stability that so many dual-income families seek in vain. The government may not be helping, but most of our financial future is in our own hands, and following the traditional rules of life are the key to that future. (Gee, sounds like Proverbs!)

* Derived by subtracting all the other figures

Labels: families, family values

posted by CPA at 10:24 AM

![]()

<< Home